Rising ROE: Japan's New Phase

The Japanese stock market is on the cusp of a significant shift, presenting a compelling opportunity for investors. Historically, low P/B ratios have plagued many Japanese companies, reflecting a market view that they were more likely to erode rather than enhance asset value. However, this perception is beginning to change.

Driven by four key levers and bolstered by four underlying catalysts, there's an emerging potential for improved ROE.

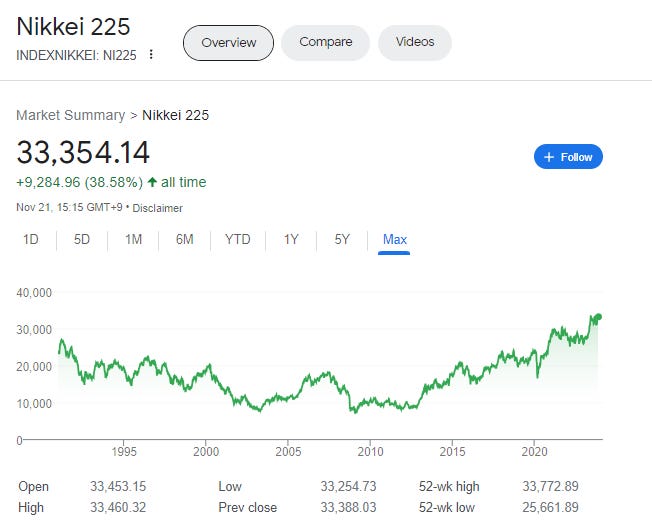

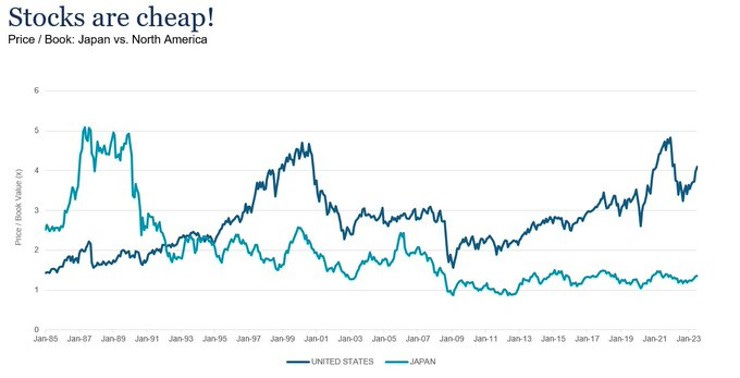

The Japanese stock market has recently reached record-high levels since the 1990s bubble burst. However, this does not mean that Japanese stocks are overvalued. On the contrary, they are still trading at a significant discount to their global peers on a P/B basis. This reflects the historical perception that Japanese companies are less efficient and profitable than their counterparts in other developed markets. However, this perception is changing as Japanese companies are undergoing a fundamental transformation in their corporate governance and management practices.

Japan’s corporate governance has evolved from a stakeholder-oriented model to a more shareholder-friendly one. The keiretsu system, which was based on cross-shareholdings and business relationships, has declined due to economic, regulatory, and market factors. Japanese companies have adopted more shareholder-friendly elements, such as board restructuring, independent directors, disclosure, capital efficiency, and sustainability.

2014: Stewardship Code established, guiding institutional investors to foster long-term company growth through active engagement and informed voting.

2015: Introduction of the first Corporate Governance Code, setting basic governance standards for listed companies in Japan to improve openness, fairness, and responsibility.

2018: Corporate Governance Code update, incorporating new rules on board freedom, diversity, sustainability, and interaction with shareholders.

2021: Further updates to the Corporate Governance Code, heightening the criteria for board independence and diversity, along with ESG reporting.

2022: Tokyo Stock Exchange reclassifies market segments into Prime, Standard, and Growth, based on distinct criteria company size, governance, and liquidity.

2023: Tokyo Stock Exchange calls on companies with low P/B ratios to focus on capital costs and share price in management, and to report on their improvement plans and progress.

In our view, the main opportunity in Japan's stock market is in buying undervalued stocks with low P/B ratios relative to ROE. If companies can improve their ROE, it could lead to a higher valuation of these stocks. This approach offers a low-risk investment option with the potential for significant returns as the ROE increases.

As we explore the potential for enhancing ROE in Japan, it's important to focus on four key 'levers' that could drive this improvement. These levers hold the promise of not only raising ROE but also contributing to a positive re-evaluation of P/B ratios.

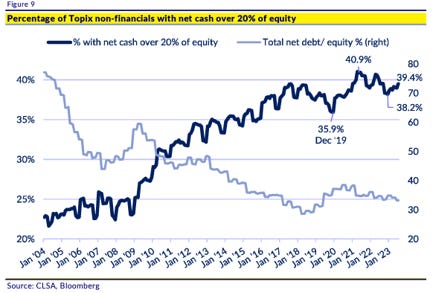

Lever 1: Companies holding significant cash reserves are being motivated to use these funds to enhance shareholder returns. This can be achieved through methods such as distributing dividends or executing share buybacks, directly benefiting shareholders and potentially increasing the company's ROE.

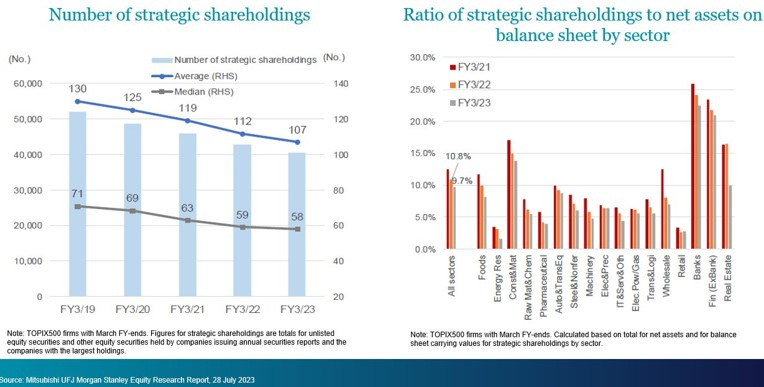

Lever 2: Companies are encouraged to assess their asset portfolio critically and divest non-core assets such as cross-shareholdings. The capital freed from such divestments can then be redirected to more profitable ventures. This strategic reallocation not only streamlines operations but also aims to boost overall returns.

Lever 3: Efforts are being made to restructure company operations by consolidating and optimizing their portfolios. This approach focuses on enhancing efficiency and profitability, which, in turn, can contribute to higher margins and an improved ROE.

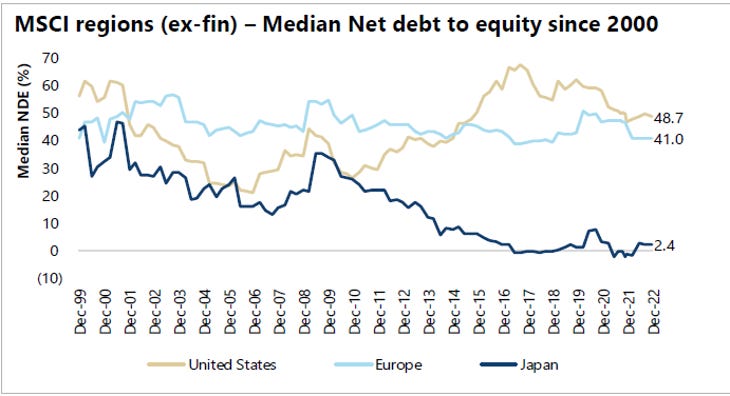

Lever 4: Firms with low leverage are advised to consider using more debt strategically. By using debt to fund growth, these companies can potentially increase their profitability and, consequently, their ROE.

Next, it's important to identify the catalysts that are prompting Japanese companies to adopt these four ROE-enhancing levers. While the value of ROE and good corporate governance has been known, there are now specific driving forces behind the more active implementation of these strategies.

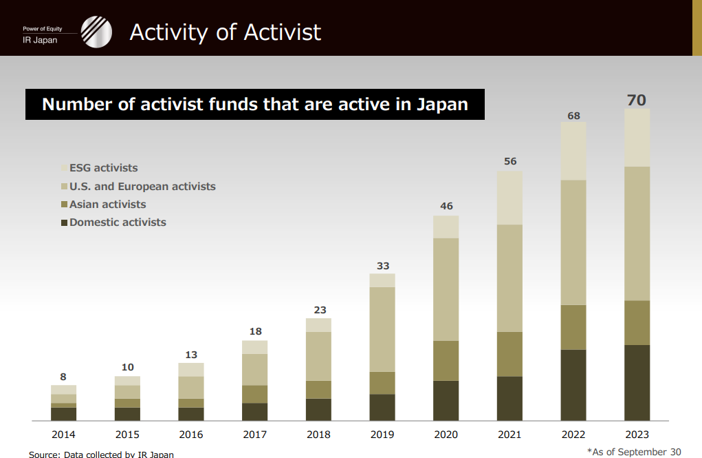

Catalyst 1: There's a growing trend of increased shareholder activism, which is exerting pressure on companies to prioritize shareholder value and undertake corporate governance reforms.

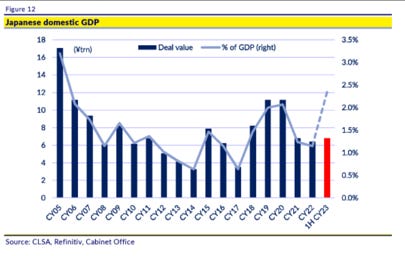

Catalyst 2: The increase in mergers, acquisitions, and takeover activities is compelling companies to refine their operations and concentrate on their core business areas.

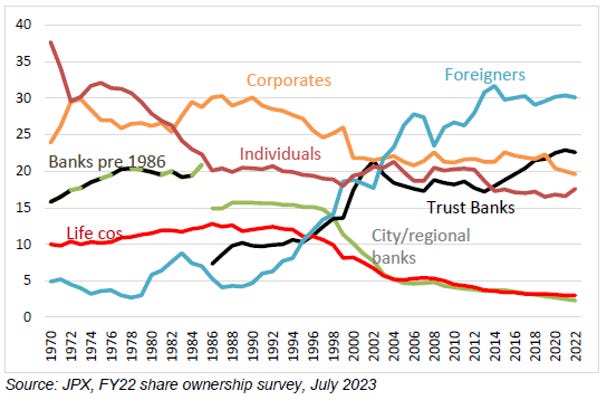

Catalyst 3: Changes in the composition of shareholders, especially with a rise in foreign investors, are driving companies towards more transparent and efficient corporate policies.

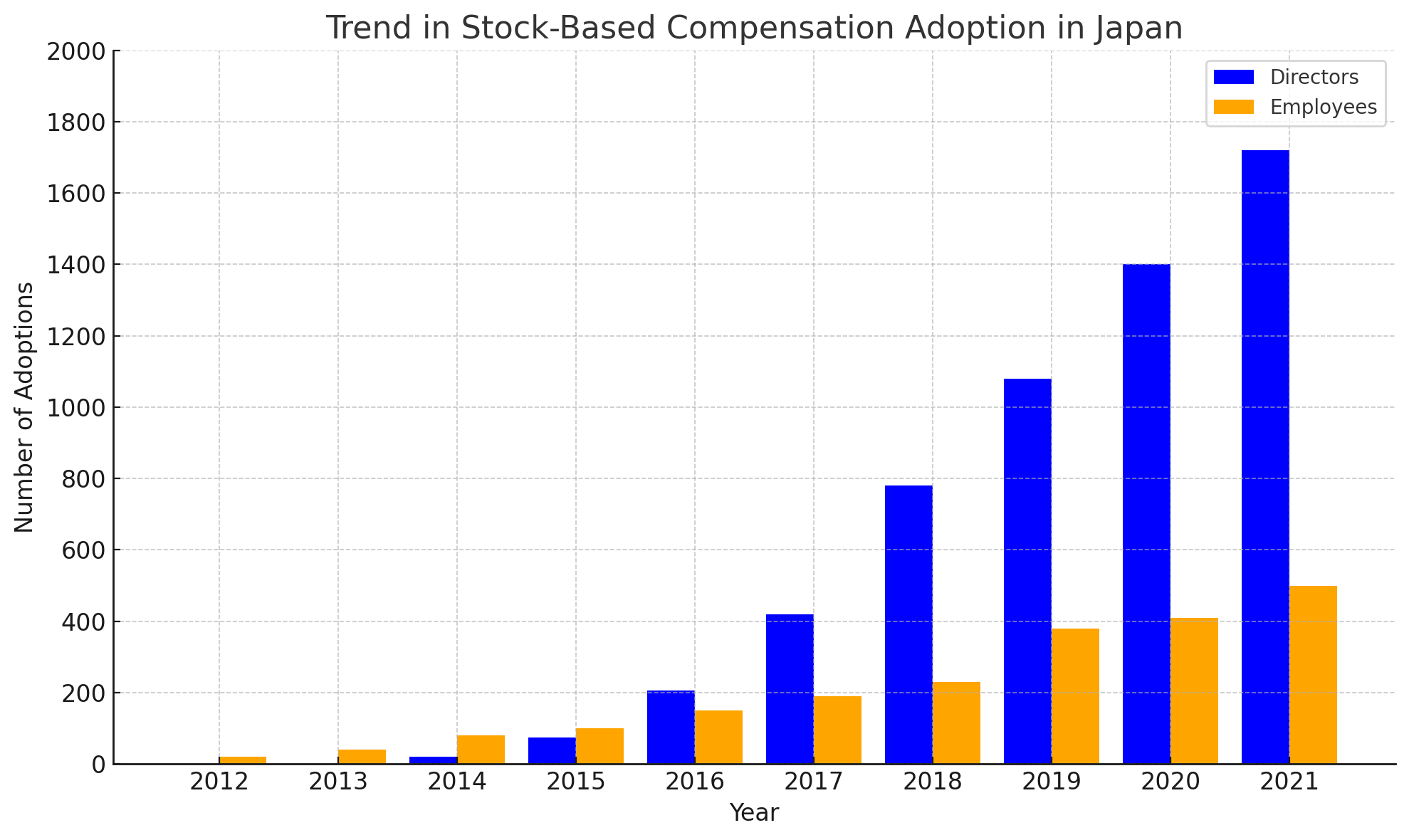

Catalyst 4: The growing implementation of stock-based compensation is increasingly aligning the interests of management with those of shareholders.

In summary, Japan's stock market is undergoing a significant shift in perception. Historically, Japanese companies were often seen as diminishing asset value, reflected in their low P/B ratios. This view is evolving, thanks to effective strategies enhancing ROE and key market catalysts. Consequently, we can anticipate a re-assessment of P/B ratios, indicating a transition from expectations of value destruction to value creation.

Credit: Most of the images above have been gathered from the twitter feed of the Fund Manager for Platinum AM's Japan strategies, Jamie Halse, which can be accessed here.

Reference for Further Reading

Hiromi Yamaji: The Banker Turned Stock Exchange Boss Rattling Japan’s Listed Companies - FT

Japan Stock Exchange Adopts Name and Shame Regime to Boost Corporate Valuations – FT

M&A among Japanese Companies Jump 80% in Domestic Restructuring Push – Nikkei

Japan’s Companies Consider Shedding Property to Boost Value - Nikkei

Japan Embraces Management Buyouts as Pressures Mount at Listed Groups – FT

Sony, Renesas Join Shift Toward Employee Stock Benefits in Japan - Nikkei

Thanks for writing this substack. Looking forward to learning more.

Hey Teddy

Great work that you are doing.

I work at Smartkarma, heard about you from there.

Can you let me know your 2 cents on Asagami Corp (9311 T). Does it really have so valuable real estate as claimed?

Thanks in advance man.